Non-listed real estate performance: Asset to Fund Level

The bigger picture

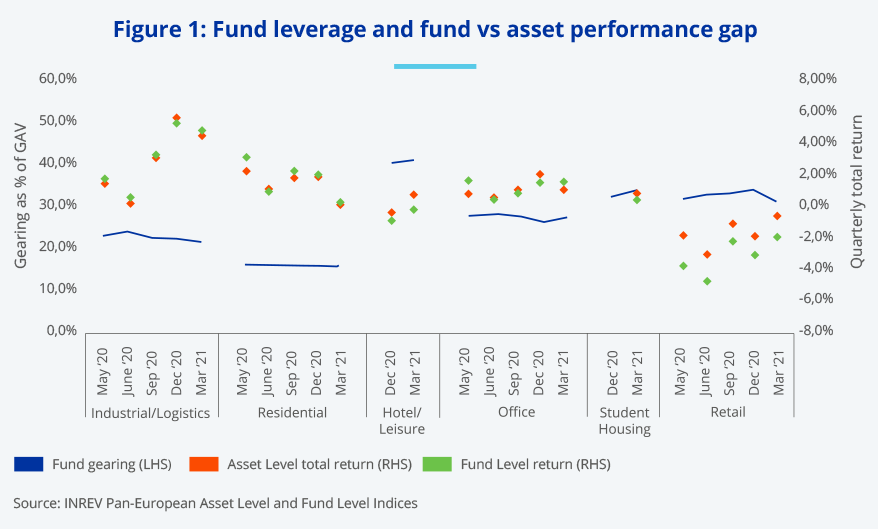

INREV is reporting on both asset and fund level performance with the INREV Asset Level Index measuring the unlevered performance of properties, portfolios, and national markets and INREV Fund Indices measuring the performance of unlisted real estate investment funds.

When thinking of asset level performance, we tend to generally refer to unlevered property returns that are derived from income and capital components. The fund level performance, on the other hand, is built up from the property level return overlaid with financials within the fund structure (debt, cash, cost and liabilities etc.) to produce an overall investment return. What is clear is that the asset and fund level performance are not comparable on a like-for-like basis as one is a component of the other. So what do the latest INREV Indices show us?

When thinking of asset level performance, we tend to generally refer to unlevered property returns that are derived from income and capital components

What do the latest INREV Indices show us?

The overall European non-listed real estate market has weakened in the last 12 months to March 2021 due to the COVID-19 pandemic, but the pandemic has hit certain sectors more than others. Retail and hospitality have been hit the hardest due to the lockdowns and restrictions reducing footfall, whereas industrials have continued to perform well as demand for home deliveries thrived, leading to some of the largest spreads in returns in history.

When comparing the asset and fund level returns, one can see a gap in the performance. It is most prominent for the retail sector, which in the last 12 months returned -6.5% at the asset level and -11.5% at the fund level. So, what is causing this performance gap? One key factor is that the higher leverage levels in the retail sector are magnifying the underperformance. Furthermore, with retail values declining sharply and rental income under pressure, this has led to increasing fund costs associated with debt refinancing, provisions on rental concessions and bad debt write-offs, all contributing negatively to the fund performance. With this in mind, we can certainly identify some of the key factors behind the difference in asset and fund performances, but it is not easy to evaluate and measure the full impact without reconciling the performance from asset to fund level.

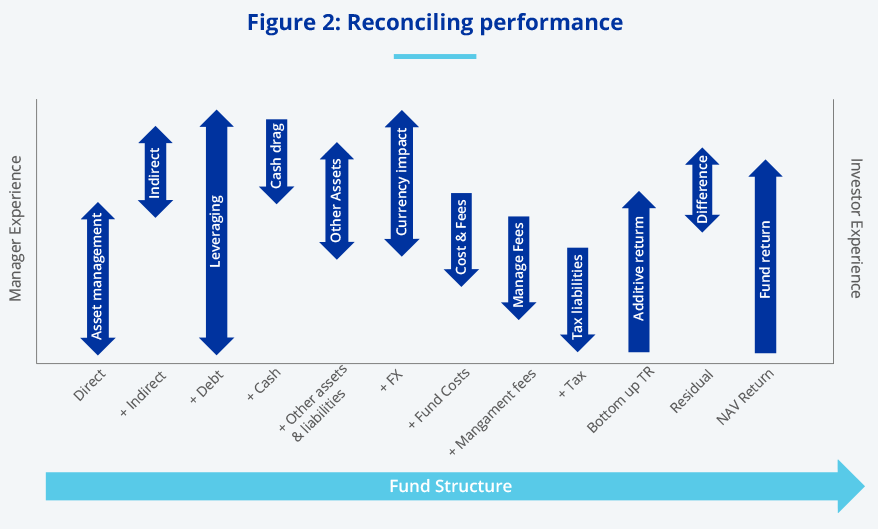

Asset to fund level performance reconciliation provides full transparency and understanding of the factors impacting the investment return and helps to align the performance between the fund manager and the investor.

The reconciliation analysis measures the impact of each of the financial layers within the fund structure against the overall investment return. Starting at the asset level each of the financial layers are added to calculate an additive return and the arithmetic difference between each layer’s additive return is used to determine the impact. The bottom-up addictive return is then comparable to the fund return and the arithmetic difference between the two is the residual. The residual difference will not always equate to zero due to the weightings and timing of cashflows e.g., amortisation, monthly-weighted vs. daily weighted cashflows.

Asset to fund level performance reconciliation provides full transparency and understanding of the factors impacting the investment return and helps to align the performance between the fund manager and the investor

Standardisation for relative performance

Managing and collating non-listed real estate data can be difficult and demanding at times, particularly as the industry becomes more regulated and the demand for data increases. By standardising performance data we can define the data requirements, provide greater transparency, and help to build a stronger framework for data governance and quality control.

In turn, having standardised data definitions and a uniformed calculation methodology the non-listed real estate industry can start thinking about measuring the attribution analysis on a relative basis. Using an industry standard such as INREV’s asset and fund calculation methodologies and pairing them with INREV’s NAV guidelines to define the financial layers would be the first step to ensuring the reconciliation analysis is comparable on a relative basis.

It is also important to note when trying to reconcile performance for a peer group the criteria for fund type, investment style and accounting standard should be also aligned. Furthermore, different calculation methodologies may also be relevant for different fund types.

It is essential the real estate industry adopts global data definitions and global methodology standards to align administrators, contributors, and users, so please support INREV in their next steps towards building greater transparency for the European non-listed real estate industry.

This article was written by Hoang Pham, Performance Director, Nuveen Real Estate and Member of the INREV Performance Measurement Committee since 2021