Meaningful progress on environmental investment underwriting

Establishing a framework to better analyse the impact of environmental capex on asset values remains high on the priority list for many market participants. At the start of 2025, INREV assembled the Environmental Underwriting Focus Group to examine the issue more closely. IQ spoke to Constantin Sorlescu, INREV’s Director of Professional Standards and Sustainability, about what’s been learned so far and what needs to happen next.

Environmental factors impacting underwriting

Objective evidence points clearly to the fact that environmental factors have become important to the process of investment underwriting. There’s also increasing pressure to meet growing regulatory and reporting requirements.

“Historically, market participants have adopted very different approaches when it comes to defining, evaluating and applying environmental factors,” says Constantin Sorlescu.

INREV, together with the focus group, has therefore embarked on developing a more consistent approach for evaluating the impact of environmental capex on value and making this easily comparable across individual assets and portfolios at a fund level.

The breadth and complexity of the topic dictated a detailed and methodical approach, focused on two major phases of investigation.

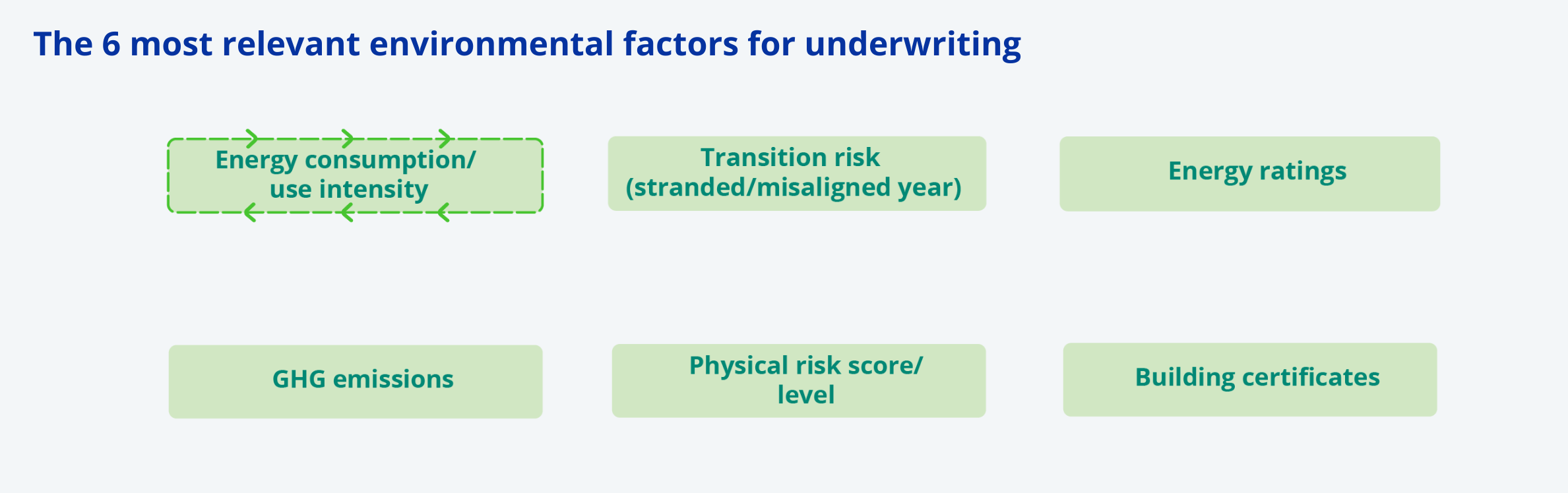

Concrete outputs

In April 2025, INREV published the initial output, which identified the six most relevant environmental factors affecting real estate investment underwriting. Selected from a long list of possible candidates, these factors are energy consumption, energy ratings, GHG emissions, stranded / misaligned (climate transition) year, physical climate risks, and building certifications.

Source: Integrating environmental considerations into real estate underwriting, INREV

The second phase of activity shifted into practical territory. ‘By overlaying the six key factors onto a DCF model and applying this to real-life case studies, we’ve now been able to gather a much more precise understanding of how environmental data can be integrated into underwriting, and how these factors impact asset management decision making,” comments Constantin.

Critically, the adapted DCF-based model reflected real capex interventions as well as data typically required for the valuation of assets in core sectors, including office, logistics, residential and retail. These inputs were used to reconcile asset values before and after intervention. The investment analysis approach was made practical by starting with the all-important payback period, calculated from cash flows tied to environmental improvements.

Above all, this exercise unearthed two important insights. The first is that, of the six key environmental factors, energy efficiency has the clearest traceable effect on payback. Secondly, it highlighted the tension between long-term environmental ambitions and short-term investment goals and the fact that shifts in valuations can’t be unequivocally attributed to environmental factors alone.

It also evidenced various limitations. Data gaps and differing views on what constitutes environmental capex, for example, continue to pose challenges for comparison and financial modelling.

More to do

INREV has responded to the industry’s call for clearer quantification in investment analysis, yet a complete answer to a one-size-fits-all methodology for valuing environmental factors consistently remains an evolving area. This analysis is inherently asset-specific – each property has its own story, shaped by its business plan and strategy. Larger datasets are needed to strengthen evidence-based underwriting for environmental inputs and demonstrate how these explicitly influence value.

‘We’re moving in the right direction,” concludes Constantin. ‘But building momentum from this point will rely heavily on the industry’s collective willingness and ability to collate and share better quality data, align more closely on key definitions, and be more upfront about assumptions.’

There’s also a pressing need for greater collaboration between valuers, managers and investors around a consistent assessment of environmental performance. INREV will continue engaging with industry stakeholders and collaborating with other bodies, such as RICS and ULI, working towards a set of best practices for real estate investment professionals.

So, while the direction of travel and ultimate destination are now clear, it’s equally evident that this objective still has some way to go.