-

Source: -

-

Source: -

-

Source: -

-

Source: -

No about page exists.

For the disclosure of the INREV TGER and REER a calculation based on INREV GAV is required.

In using/preparing the INREV TGER and REER the question might arise about which components should be included in calculating the (INREV GAV) denominator of these ratios.

The fund manager should be transparent in its reporting to investors and explain the methodology and assumptions used for the calculation of the GAV, as required by both INREV NAV and Fee and Expense Metrics modules.

The Total Assets derived from Generally Accepted Accounting Principles (GAAP), including IFRS, could be used as a starting point in the calculation of the denominator of the ratios presented in the Fee and Expense Metrics module.

INREV suggests to start from the same accounting framework as it was used in calculating the INREV NAV, i.e., IFRS, local GAAP or other vehicle specific GAAP.

From there, the various adjustments should be included, or excluded, to come to an INREV GAV that can be used in the calculation of the INREV TGER and REER.

In preparing this Q&A the guidance provided to the users should be read in light of the requirements included in the Fee and Expense Metrics module.

It should be noted that the INREV GAV used for the INREV TGER and REER calculation might be different than an adjusted GAV used for performance measurement or other disclosure requirements. Additional adjustments could be included, or excluded, to come to an adjusted GAV to better suit a particular purpose.

The INREV GAV guidance overrides the accounting principles by making adjustments to the results arrived at by following the chosen GAAP.

INREV GAV adjustments require some material judgment by the manager. Consequently, it is important to include sufficient disclosures to allow investors to understand positions taken by the manager.

In this Q&A, direct links will be made to IFRS as a basis for calculating the required adjustments, and if needed, to other fair value concepts. If another basis of GAAP is used as a starting point, further adjustments may be required to align with IFRS for determining the INREV GAV. References to further guidance by INREV on the interpretation of fair value and provision accounting are also included.

For the use of calculating the INREV TGER and REER, a vehicle GAV calculated in accordance with IFRS should be adjusted for the following items:

INREV GAV adjustment table:

| Total | |

| GAV per the IFRS financial statements (Total Assets) | x |

| Fair value of assets | |

| a) Revaluation to fair value of investment properties | x/(x) |

| b) Revaluation to fair value of self-constructed or developed investment property | x/(x) |

| c) Revaluation to fair value of investment property held for sale | x/(x) |

| d) Revaluation to fair value of property that is leased to tenants under a finance lease | x/(x) |

| e) Revaluation to fair value of real estate held as inventory | x/(x) |

| f) Revaluation to fair value of other investments in real assets | x/(x) |

| g) Recognition to fair value of indirect investments not consolidated | x/(x) |

| h) Revaluation to fair value of financial assets | x/(x) |

| i) Revaluation to fair value of construction contracts for third parties | x/(x) |

| j) Set-up costs | x/(x) |

| k) Acquisition expenses | x/(x) |

| Effects of the expected manner of settlement of sales/vehicle unwinding | |

| l) Revaluation to fair value of savings of purchaser’s costs such as transfer taxes | x/(x) |

| Other adjustments | |

| m) Goodwill | x(x) |

| n) Derecognition of financial derivatives | x/(x) |

| o) Derecognition of deferred tax assets | x/(x) |

| INREV GAV | x |

Fair value of assets

a) Revaluation to fair value of investment properties

If a real estate vehicle uses the option to account for investment properties under the cost model, this adjustment represents the impact on GAV of the revaluation of the investment property to fair value under the fair value option of IAS 40.

The effect of straight-lining of lease incentives, rent guarantees, insurance claims (for damages, lost rent, etc.) should be taken into account when valuing the property at fair value in accordance with IAS 40 and SIC 15 to ensure that any asset is not double counted in the GAV.

b) Revaluation to fair value of self-constructed or developed investment property

If a real estate vehicle uses the option to account for self-constructed or developed investment property under the cost model, the adjustment represents the impact on GAV of the revaluation of the self-constructed or developed investment property to fair value under the fair value option of IAS 40.

c) Revaluation to fair value of investment property held for sale

Some investment properties may be classified as assets held for sale or as a group of assets held for sale. The carrying value of such investment properties depends on the chosen accounting treatment under IAS 40 (either fair value or cost).

The adjustment represents the impact on GAV of the revaluation of the investment property intended for sale, measured at fair value or cost, to the net realisable value (fair value less disposition costs).

d) Revaluation to fair value of property that is leased to tenants under a finance lease

Property that is leased to tenants under a finance lease is initially measured on a net investment basis and subsequently re-measured based on an amortisation pattern reflecting a constant rate of return.

The adjustment represents the impact on GAV of the revaluation of the finance lease receivable to fair value.

e) Revaluation to fair value of real estate held as inventory

Properties intended for sale and accounted for under IAS 2 (Inventory) are measured at the lower of cost or net realisable value in the financial statements. This adjustment represents the impact on the GAV of the revaluation of such properties to net realizable value (fair value less disposition costs). This adjustment should be included under the caption ‘revaluation to fair value of real estate held as inventory’.

Where the likely disposition date is more than one year from the date of the GAV computation, disposition costs should not be deducted from fair value in calculating this adjustment..

f) Revaluation to fair value of other investments in real assets

Under IAS16 other investments in real assets are normally accounted for at cost.

The adjustment represents the impact on GAV of the revaluation of other investments in real assets to fair value in accordance with the fair value assumptions under IFRS 13.

g) Recognition to fair value of indirect investments not consolidated

Indirect investments in real estate, such as investments in associations and joint ventures, have different accounting treatments and carrying values under IFRS. Such investments can be valued at cost, fair value or NAV.

The adjustment represents the impact on GAV of the recognition of indirect investments not consolidated and depending on the type of investment at fair value.

Under this adjustment, two situations can be identified:

1. Investments for which fees and costs are proportionally taken into consideration in the calculation of the fee and expense metrics

The adjustment represents the impact on GAV when including the proportional GAV of the associations and joint ventures based on the share that the vehicle holds.

In this case, all assets should be included proportionally for the share that the vehicle holds in the assets of the associations or joint venture. These assets should be valued in accordance with the guidance provided herein. All corrections should be taken into consideration and should be reflected, as applicable, when calculating the INREV GAV for the purpose of preparing the INREV TGER and REER.

2. Investments for which fees and costs are not taken into consideration in the calculation of the fee and expense metrics

The adjustment represents the impact on GAV of the revaluation of indirect investments to fair value, if not yet accounted for at fair value. Reference is made to the INREV NAV guidelines, and more specifically to Q&A-4 of the INREV NAV module.

h) Revaluation to fair value of financial assets

Financial assets are generally measured at amortised cost, taking into account any impairments (when applicable). The adjustment represents the impact on GAV of the revaluation of financial assets to fair value, as determined in accordance with IFRS, if not yet accounted for at fair value.

i) Revaluation to fair value of construction contracts for third parties

Under IAS11, construction contracts for third parties are normally accounted for based on the stage of completion.

The adjustment represents the impact on GAV of the revaluation of construction contracts for third parties to fair value in accordance with the fair value principles of IFRS 13.

Adjustments to reflect the spreading of one-off costs

As described in further detail below, set-up costs and acquisition expenses should be capitalised and amortised. The rationale for these adjustments is to spread these costs over a defined period of time to smoothen the immediate impact of costs on the vehicle’s performance. Furthermore, it is a simple mechanism to spread costs between different investor groups entering or leaving the vehicle’s equity at different times. Such adjustments are taken into account in the calculation of the ratio numerator included in the Fee and Expense Metrics module.

Since the INREV GAV is primarily intended to facilitate comparability between different vehicles, the INREV approach is a simple but stable methodology where these capitalised costs are subject to an impairment test each time the GAV is calculated and therefore should always be recoverable over time.

j) Set-up costs

Under IFRS, vehicle set-up costs are charged immediately to income after the inception of a vehicle. Such costs should be capitalised and amortised over the first five years of the term of the vehicle.

The rationale for capitalising and amortising set-up costs is to better reflect the duration of the economic benefits to the vehicle. Furthermore these costs are taken into account in the calculation of the ratio numerator included in the Fee and Expense Metrics module.

When capitalising and amortising set-up costs, a possible impairment test should be taken into account every time the adjusted GAV is calculated when market circumstances change and it is not expected that the capitalised set-up costs can be recovered through the sale of units of a vehicle. For instance, when a decision is made to liquidate the vehicle or stakeholders no longer expect to recover the economic benefit of such capitalised expenses, they should be written off.

k) Acquisition expenses

Under the fair value model, acquisition expenses of an investment property are effectively charged to income when fair value is calculated at the first subsequent measurement date after acquisition. This results in the fair value of a property on subsequent fair value measurement being lower than the total purchase price of the property, all other things being equal.

Property acquisition expenses should be capitalised and amortised over the first five years after acquisition of the property.

The rationale for capitalising and amortising acquisition expenses is to better reflect the duration of the economic benefits to the vehicle of these costs. Furthermore these cost are taken into account in the calculation of the ratio numerator included in the Fee and Expense Metrics module. When capitalising and amortising acquisition costs, a possible impairment test should be taken into account each time the adjusted GAV is calculated when market circumstances change and it is not expected that the capitalised acquisition costs can be recovered through the sale of units of a vehicle. When a property is sold during the amortisation period, or is classified as held for sale, the balance of capitalised acquisition expenses of that property should be expensed.

Effects of the expected manner of settlement of sales/vehicle unwinding

l) Revaluation to fair value of savings of purchaser’s costs such as transfer taxes

Transfer taxes and purchaser’s costs which would be incurred by the purchaser when acquiring a property are generally deducted when determining the fair value of investment properties under IAS 40.

The effect of an intended sale of shares in a property-owning vehicle, rather than the property itself, should be taken into account when determining the amount of the deduction of transfer taxes and purchaser’s costs, to the extent this saving is expected to accrue to the seller when the property is sold.

The adjustment therefore represents the positive impact on the GAV of the possible reduction of the transfer taxes and purchaser’s costs for the benefit of the seller based on the expected sale of shares in the property-owning vehicle.

Disclosure should be made on how the estimate of the amount the manager expects to benefit from intended disposition strategies has been made. Reference should be made to both the current structure and prevailing market conditions.

Other adjustments

m) Goodwill

At acquisition of an entity which is determined to be a business combination, goodwill may arise as a result of a purchase price allocation exercise. Often a major component of such goodwill in property vehicles reflects the difference between the full recognition of deferred tax, purchaser’s costs or similar items in the IFRS accounts (which does not generally take account of the likely or intended method of subsequent exit), and the economic value attributed to such items in the actual purchase price.

Except where such components of goodwill have already been written off in the GAV as determined under IFRS, they should be written off in the INREV GAV.

n) Financial derivatives

This adjustment relates to the derecognition of any financial derivatives which are reported on the asset side of the balance sheet.

This relates to all financial derivatives as interest instruments, cash flow instruments and or currency exchange instruments. The rationale is that all the expenses/charges in respect to these instruments are linked to a liability or exempted for the calculation of the ratio numerator included in the Fee and Expense Metrics module.

o) Deferred tax assets

This adjustment relates to the derecognition of any deferred tax assets which are reported on the asset side of the balance sheet. The rationale is that all the expenses/charges in respect to taxes are linked to a liability or exempted for the calculation of the ratio numerator included in the Fee and Expense Metrics module.

It may happen that some vehicles have hired employees. Related staff costs should be allocated based on the activity of the employees.

For instance, the wage and related costs of employees working on property related matters should be allocated to property expenses and therefore included in the REER.

How should fee and expense metrics be determined in case a fund manager wishes to disclose quarterly ratios?

INREV Guidelines require the computation of the fee and expense metrics on an annual basis. Fund managers may provide investors with quarterly ratios. INREV Guidelines do not propose any methodology to compute quarterly ratios.

Fund managers can indeed disclose quarterly fee and expense metrics to investors. The methodology should be consistent with the methodology used for the fee and expense metrics in the annual reports, particularly on the cost classification and computation methodology.

The quarterly metrics should be presented on a rolling four quarter basis.

The fund manager should be transparent in its reporting to investors and explain the methodology and assumptions used.

In case a fund manager discloses quarterly ratios, the fund manager is still required to disclose the annual metrics in the annual reporting to comply with requirements included in the fee and expense metrics.

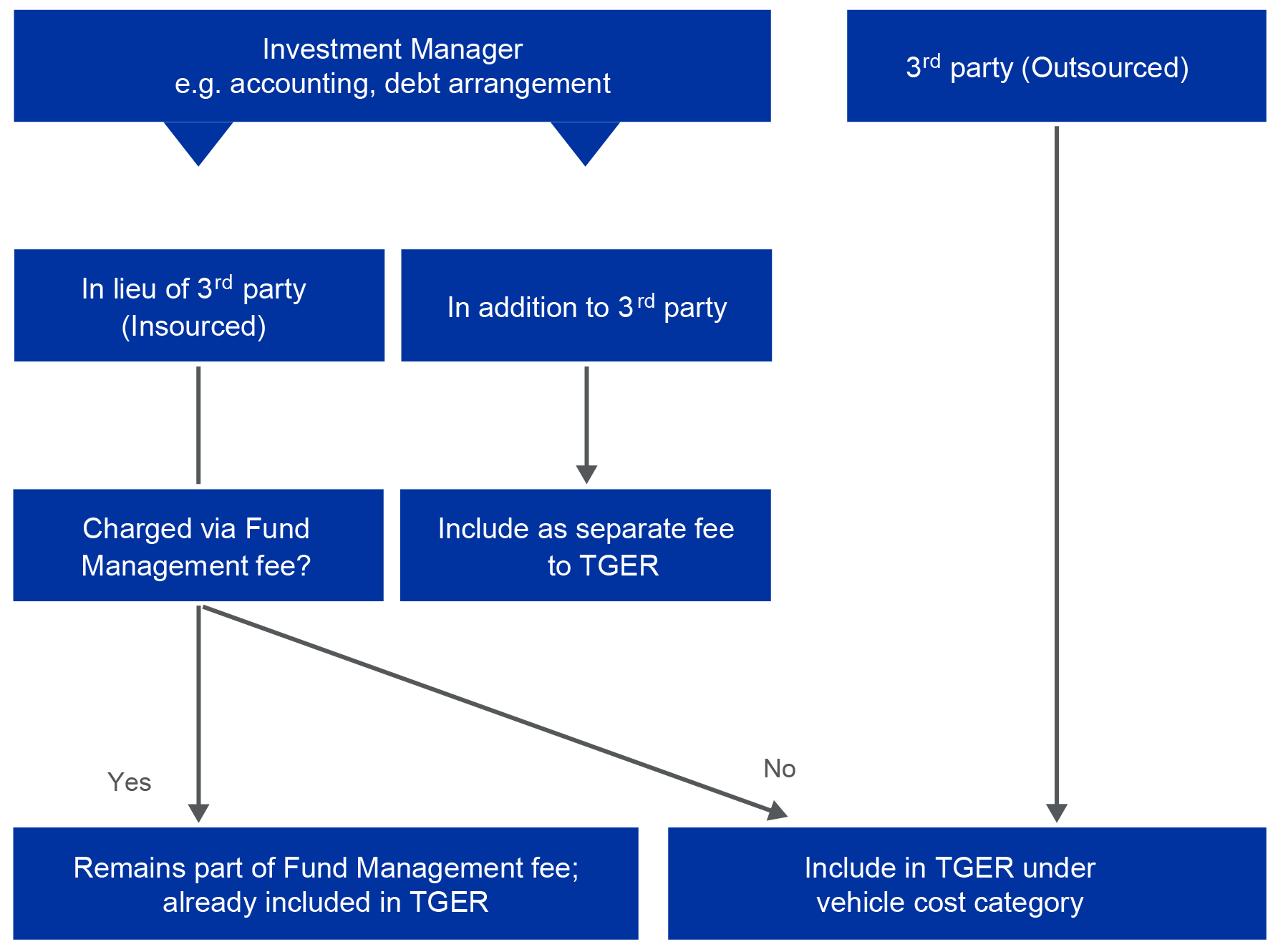

Generally, when a function and its related services is frequently outsourced to third parties and the vehicle designates the investment manager to perform this function internally, then the services provided by the investment manager are deemed to be in lieu of third-party services. Conversely, when there is already a charge from a third-party for services related to a specific function, and due to task complexity, the investment manager provides oversight or performs other complementary services for the benefit of the vehicle, then these services provided by the investment manager are deemed to be in addition to third party services.

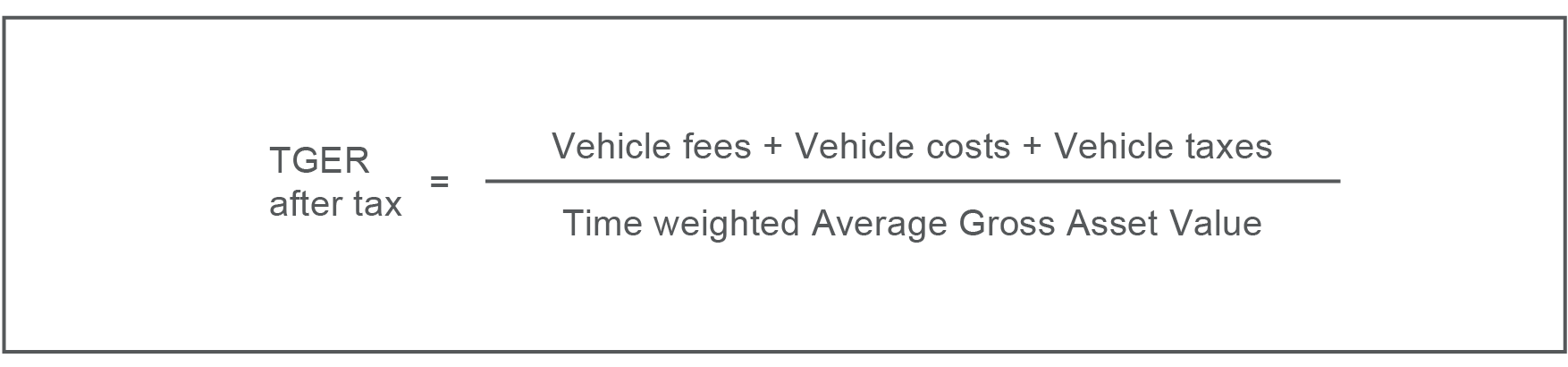

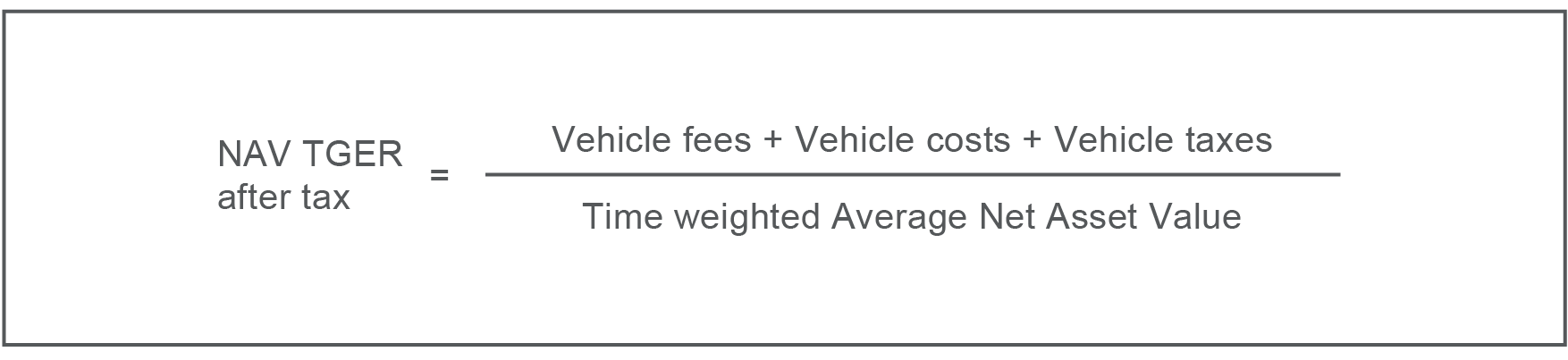

If considered meaningful, a TGER after tax may be also calculated and disclosed by the investment manager to reflect the cost associated with tax structures and taxable income.

The formulae are presented below:

Vehicle taxes included in the TGER after tax comprise:

TGER represents a natural progression from the previously reported INREV TER and includes several additional fees. A mapping of TER to TGER is summarised below, including its main components.

Conversion of previously reported TERs is not necessarily. The numerator of TGER bears much similarity to the TER. It is important to note however that historical comparisons depend on the life cycle and activity of the vehicle and should be treated with caution.

| Allocation of main fees and costs from TER to TGER | Workings |

| Asset and fund management fees | |

| Performance fees | |

| Other fees earned by manager | |

| Total vehicle fees for TER | A |

| Audit, valuation, custodian, transfer agent and other admin costs | |

| Vehicle formation costs and dead deal costs | |

| Bank charges and other professional service costs | |

| Total vehicle costs for TER | B |

| Adjustments for TGER | |

| Property acquisition and disposition fees | |

| Project management fees | |

| Debt arrangement fees and costs | |

| Fee and costs adjustments for TGER | C |

| Vehicle taxes (optional, for after-tax TGER calculation) | |

| Vehicle tax adjustments for TGER | D |

| Time-weighted average GAV | E |

| Time-weighted average NAV | F |

| Required ratio: TGER | (A+B+C)/E |

| Recommended ratio: NAV TGER | (A+B+C)/F |

| Optional ratio: (NAV)/TGER after tax | (A+B+C+D)/E or(F) |

TGER was designed to consider all relevant elements of a non-listed real estate vehicle load – including both fees and costs. Care should be taken to ensure an “apples to apples” comparison of similar measures disclosed for public markets / listed real estate investments as several adjustments may be required in case of listed structures, e.g. overhead expenses may be structured differently.

Certain services under the Asset Management fee are not included in the TGER as they are directly attributable to the building and thus still part of the REER. These may include managing of capex, management of leases, refurbishment design, management of construction progress, etc. The investment manager should use best judgement to split its asset management fee services between what is directly attributable to the building and the vehicle management activities, e.g. strategic input, production of asset level business plan.

The reporting periods for compliance with TGER are presented in the table below. TGER disclosures will be required for reporting periods ending on or after 31 December 2020. Whilst the TER remains an optional disclosure for investment managers beyond this date, its disclosure will cease to form part of INREV Adoption and Compliance Framework from reporting periods ending on or after 31 December 2020. Nevertheless, next to TGER, managers may choose to continue calculating and disclosing a TER figure on a temporary basis if considered meaningful for historical comparison.

|

INREV expense ratio reporting period |

Period/Year ended 31 Dec 2020 |

Fiscal year ended 31 Mar 2021 |

Fiscal year ended 30 Jun 2021 |

Fiscal year ended 30 Sep 2021 |

Period/Year ended 31 Dec 2021 |

|---|---|---|---|---|---|

| TGER | Required | Required | Required | Required | Required |

| TER | Optional | Optional | Optional | Optional | Optional |

In addition, managers have the option to also compute and disclose TGER on a quarterly basis (annualised), starting with Q4 2020 reporting periods. The approach should be consistent with the fee and cost allocation and computation methodology on an annual basis.

For the Total Global Expense Ratio (TGER), vehicle expenses are classified into Vehicle Fees and Vehicle Costs. As a result, the Debt Arrangement Fees charged by the investment manager for services rendered in arranging debt financing are allocated to the Vehicle Fees category. The Debt Arrangement Costs paid to a lender, broker, or other third party are allocated to the Vehicle Costs category.

As indicated in the INREV NAV and the INREV GAV Q&As, all debt arrangement fees and costs are accounted for at amortised cost and these costs are then charged via amortisation to Profit and Loss over the term of the loan.

A parallel should also be made to the Property Acquisition Fee and the Property Acquisition Cost, as their amortisation for the period/year is included in the calculation of TGER.

It follows that for both Debt Arrangement Fees and Costs, the amortisation for the period/year should be included in the calculation of TGER.