-

Source: -

-

Source: -

-

Source: -

-

Source: -

No about page exists.

Fees and costs should be measured in line with the principles defined under INREV NAV and INREV GAV.

Fees describe charges borne by the vehicle for services provided by the manager and costs describe charges to a vehicle by external service providers. Fees charged by the manager directly to their investors are not taken into account, with the exception of fees charged for services rendered to the vehicle.

Where a single fee is charged to cover a variety of activities, the constituent elements will need to be identified, allocated to the appropriate cost category and disclosed appropriately.

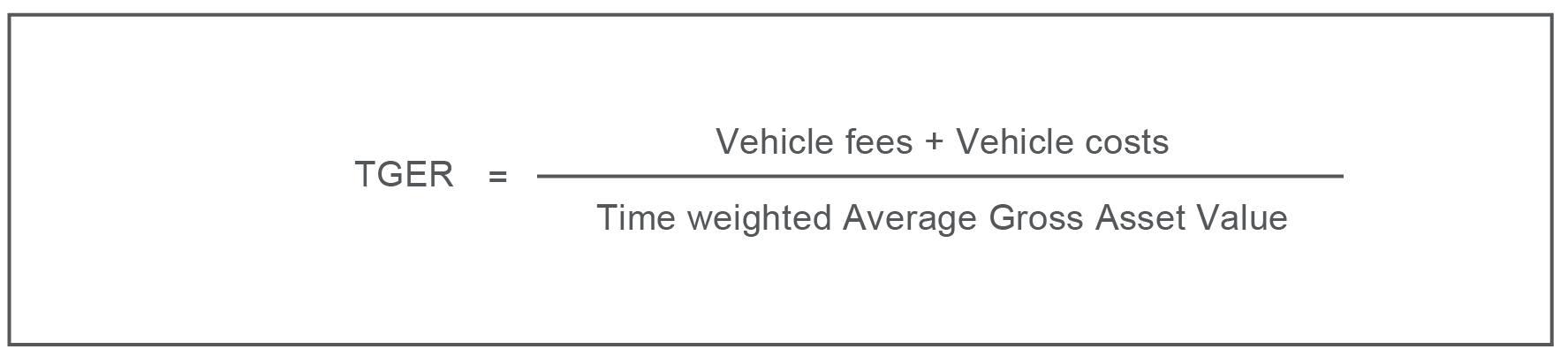

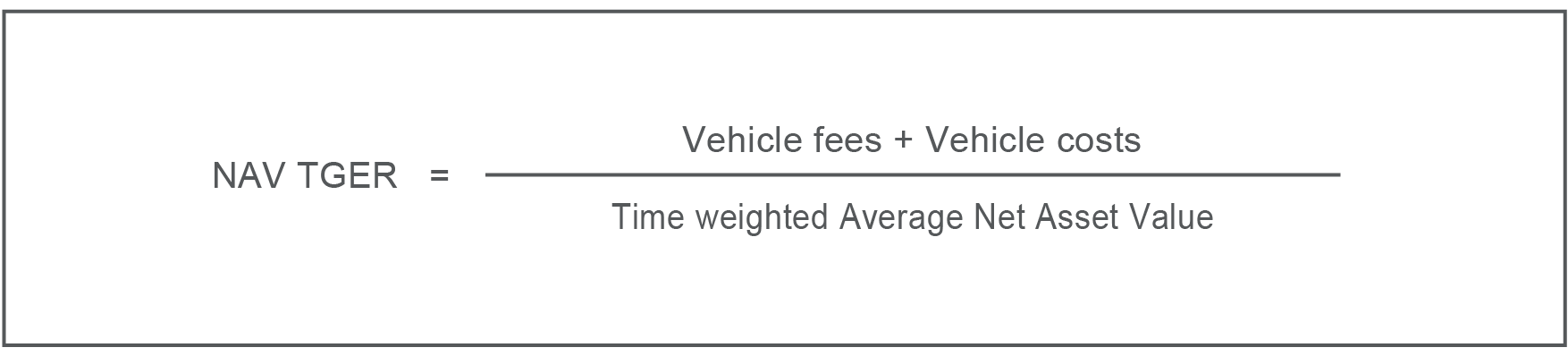

Historic Total Global Expense Ratio

A historic TGER, based on the time-weighted average INREV GAV of the vehicle over twelve months, should be provided annually.

This approach removes the effect of leverage and provides a more relevant comparison between investment vehicles with different capital structures. Depending on the investor needs, investment managers may also provide a historic NAV TGER based on the time-weighted average INREV NAV.

If considered meaningful, managers may compute and disclose TGER on a quarterly basis (annualised), since inception, or on rolling multiple period averages. The approach should be consistent with the fee and cost allocation and computation methodology on an annual basis.

For the calculation methodology, daily weighting of cash flows is recommended. If not feasible, at a minimum, quarterly figures should be used to calculate the time weighted average INREV GAV and INREV NAV.

The components of the numerator include the vehicle fees and costs for the reporting period, as defined below.

Certain fees and costs, such as property-level costs charged by the manager, should not be included when calculating the TGER; they do however form part of the REER (see below). If the manager charges a single fee covering both property and vehicle management activities, it should be split into its constituent elements.

The formulae for TGER are:

The TGER is an historic or ‘actual’ figure, based on data published annually. Consequently, newly launched vehicles cannot have an historic TGER.

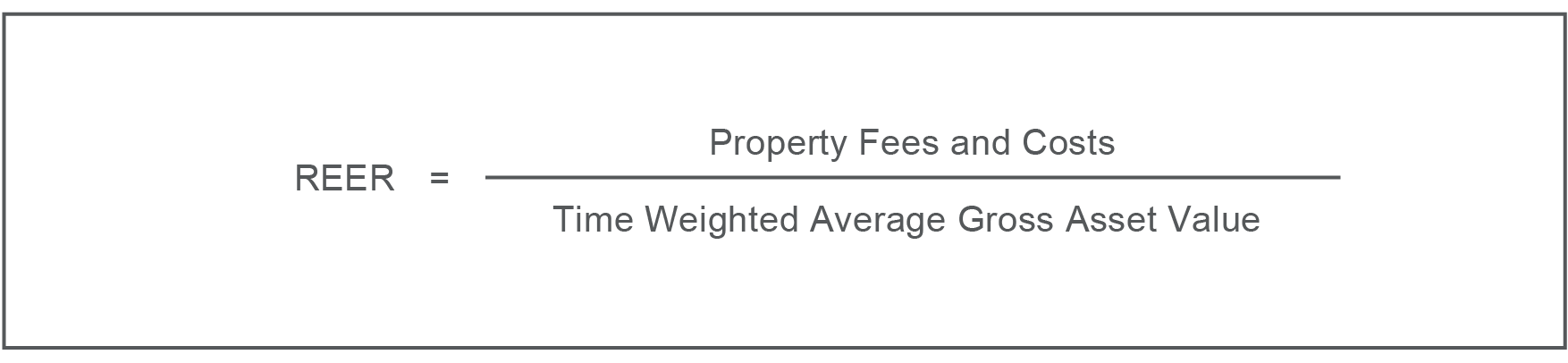

Historic Real Estate Expense Ratio

An historic REER, based on the time-weighted average INREV GAV of the vehicle over twelve months, should be disclosed annually.

While the TGER relates to the operating costs borne by the vehicle, the REER captures only those costs that relate to the management of the real estate assets. The REER includes the property-specific costs described below.

The numerator should include the fees and costs associated with managing the properties, while the denominator should be the time-weighted average INREV GAV.

The formula for REER is:

Forward-looking ratios

Forward-looking ratios and metrics are useful items in the vehicle documentation. However, they are ‘theoretical’, in that they are based on estimated costs, anticipated numbers of assets, and assumptions such as growth rate, vehicle life and tax structuring. Requirements for forward-looking fee and expense metrics at the vehicle launch stage are described below. Once the vehicle has commenced operations, there should be no further requirement for forward-looking metrics as historic metrics based on historic data should then be available.

Forward-looking Total Global Expense Ratio

A forward-looking TGER, based on the time-weighted average INREV GAV for the first year when the vehicle is expected to be stabilised, should be provided in the vehicle documentation. A forward-looking NAV TGER based on the time-weighted average INREV NAV may also be provided. These measures should be calculated following the same methodology as for a historic TGER and for NAV TGER, although they will be based on estimates.

The forward-looking TGER and NAV TGER should be accompanied by disclosure of the estimates used to calculate this metric.

Forward-looking real estate expense ratio

A forward-looking REER, based on the time-weighted average INREV GAV of the vehicle for the first year when the vehicle is expected to be stabilised, should be provided in the documentation. This should be calculated following the same methodology as for an historic REER, although it will be based on estimates.

The forward-looking REER should be accompanied by a disclosure of the estimates used to calculate this metric.